What Actually Moves a Stock Before Earnings?

A clearer way to understand the forces shaping stock prices before earnings season arrives.

A lot of investors think stocks move on earnings day because the numbers come in above or below expectations.

That is true sometimes.

But it misses what usually happens first.

Most of the move starts before the report.

By the time earnings day arrives, the market has already spent days or weeks adjusting to clues. Analysts update models. Investors react to competitor results. Management teams hint at pressure or strength. The stock starts moving before the company ever says a word on the call.

That is why the better question is not, “What will the company report?”

It is, “What is the market already starting to believe?”

The market does not wait for the final answer

Stocks are forward-looking. That sounds obvious, but it matters most around earnings.

The market is not just reacting to last quarter’s revenue or EPS. It is trying to price what the quarter means for the next one. That includes whether demand is improving, whether margins are holding up, whether guidance is about to rise or fall, and whether the story around the business is getting better or worse.

In other words, earnings season is not just about the number.

It is about the setup around the number.

That setup is what moves the stock before the report arrives.

What investors are actually watching

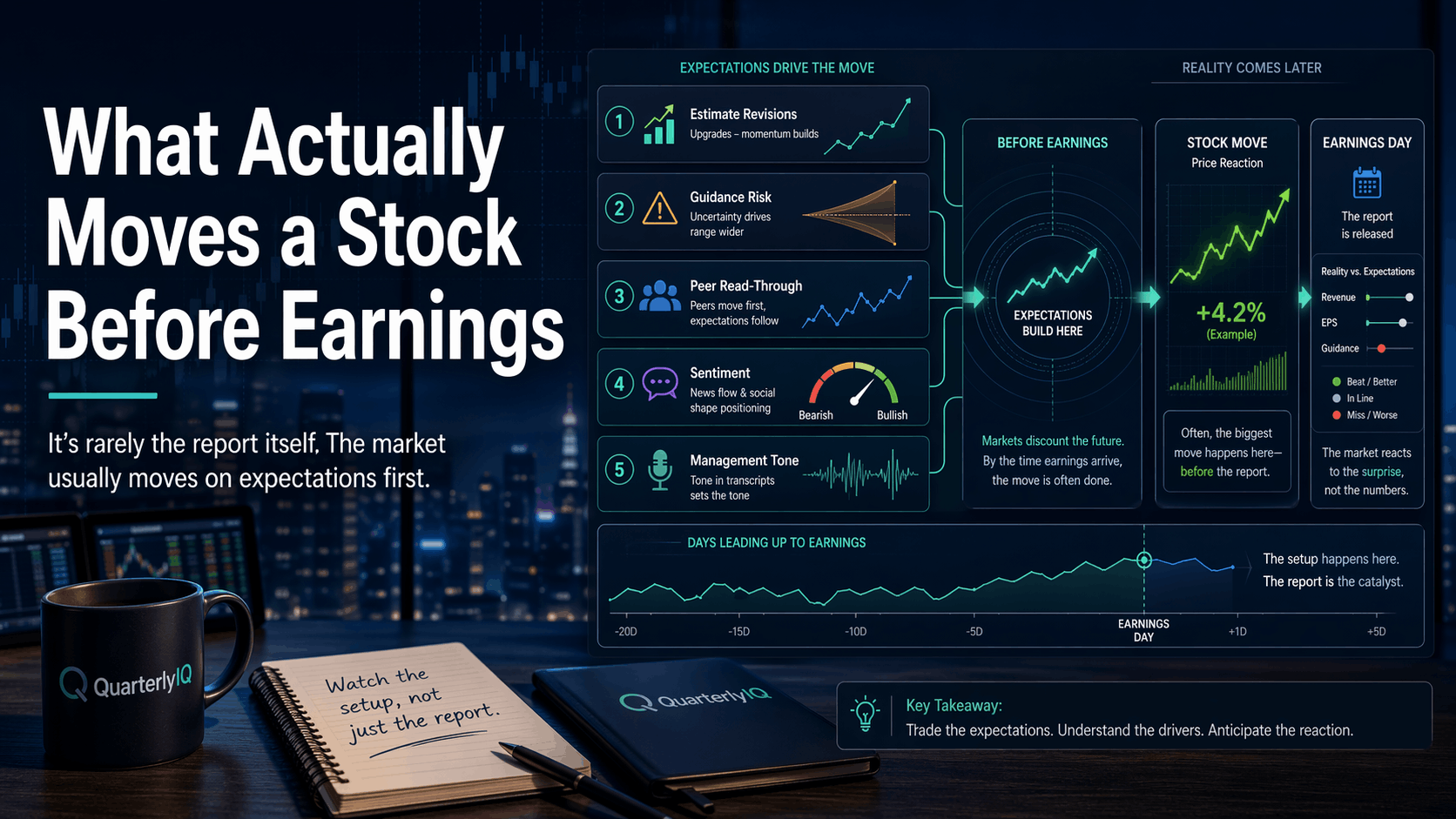

Before earnings, there are usually five things doing most of the work.

1. Estimate revisions If analysts are raising numbers ahead of the report, the bar is moving higher. If they are cutting numbers, the bar is getting lower. That changes what counts as a surprise.

2. Guidance risk Sometimes investors care less about the quarter that is ending and more about what management is about to say next. A company can post solid results and still fall if guidance looks soft.

3. Peer read-through One company often gives clues about another. If a competitor talks about weaker demand, pricing pressure, or slowing orders, the market may start pricing that risk into the whole group.

4. Sentiment and positioning If the stock has already rallied hard into earnings, expectations may be too high. If sentiment is weak and the stock has already been hit, the setup may be easier. That is why the same report can get a very different reaction depending on where the stock started.

5. Management tone Sometimes the most important signal is not in the press release. It is in how management sounds. Investors listen for confidence, hesitation, caution, and changes in language. A subtle shift in tone can matter more than a small beat.

This is exactly the kind of setup QuarterlyIQ should help investors see early: not just the report date, but the expectations, pressure points, and watch items already building around it.

Why this matters more than the headline

This is where investors get tripped up.

They see a headline like “Company beats earnings estimates” and assume the stock should rise.

But a beat only matters in context.

If the market already expected a strong quarter, a normal beat may not be enough. If the stock ran up into earnings, investors may want a bigger surprise. If guidance is flat, margins look soft, or management sounds cautious, the stock can fall anyway.

On the other hand, a company can miss and still rise if expectations were already low and the report shows the damage is not as bad as feared.

That is the part that matters most.

Stocks move on the gap between expectations and reality, not on the headline in isolation.

What this means for sectors and stocks

This gets even more important at the sector level.

If a whole sector has been getting upbeat commentary, rising estimates, and stronger price action, then the group may enter earnings season with very little room for disappointment. In that setup, even decent results may not be enough.

If a sector has been weak, estimates have been cut, and sentiment is already poor, the opposite can happen. A merely okay quarter can feel like relief.

That is why pre-earnings moves are often telling you something useful. The market is showing you where optimism or fear is already building.

Not perfectly. But often early.

What to watch before the next report

Before the next company on your watchlist reports, ask a few better questions.

Are estimates moving up or down?

What have peers already said?

Has the stock already moved like good news is coming?

What does management need to prove this quarter: growth, margins, guidance, or demand?

Those questions will usually tell you more than waiting for the headline.

Bottom line

What actually moves a stock before earnings is not the report alone.

It is the setup.

It is the revisions, the whispers, the peer signals, the guidance risk, and the feeling that the market is already leaning one way or the other.

By earnings day, the stock is often not reacting to the quarter itself.

It is reacting to whether reality was better or worse than the version of the quarter investors had already built in their heads.

That is where the real signal usually hides.

Follow QuarterlyIQ for more plain-English breakdowns on the economy, sectors, and stocks, and to track the setup before the headline hits.