What GDP, PCE, and Jobless Claims Are Telling Us Right Now and Why Policy May Follow

Growth is slowing, inflation is easing, and labor remains stable. Here’s what the latest data signals for markets and Fed policy heading into May.

The latest macro data did not introduce a new narrative. It confirmed what has been building for months.

Growth is slowing. Inflation is gradually easing. The labor market is still holding firm.

Individually, these signals matter. Together, they define the current economic setup heading into May.

QuarterlyIQ is designed to detect this kind of transition early.

GDP: Growth Is Moderating

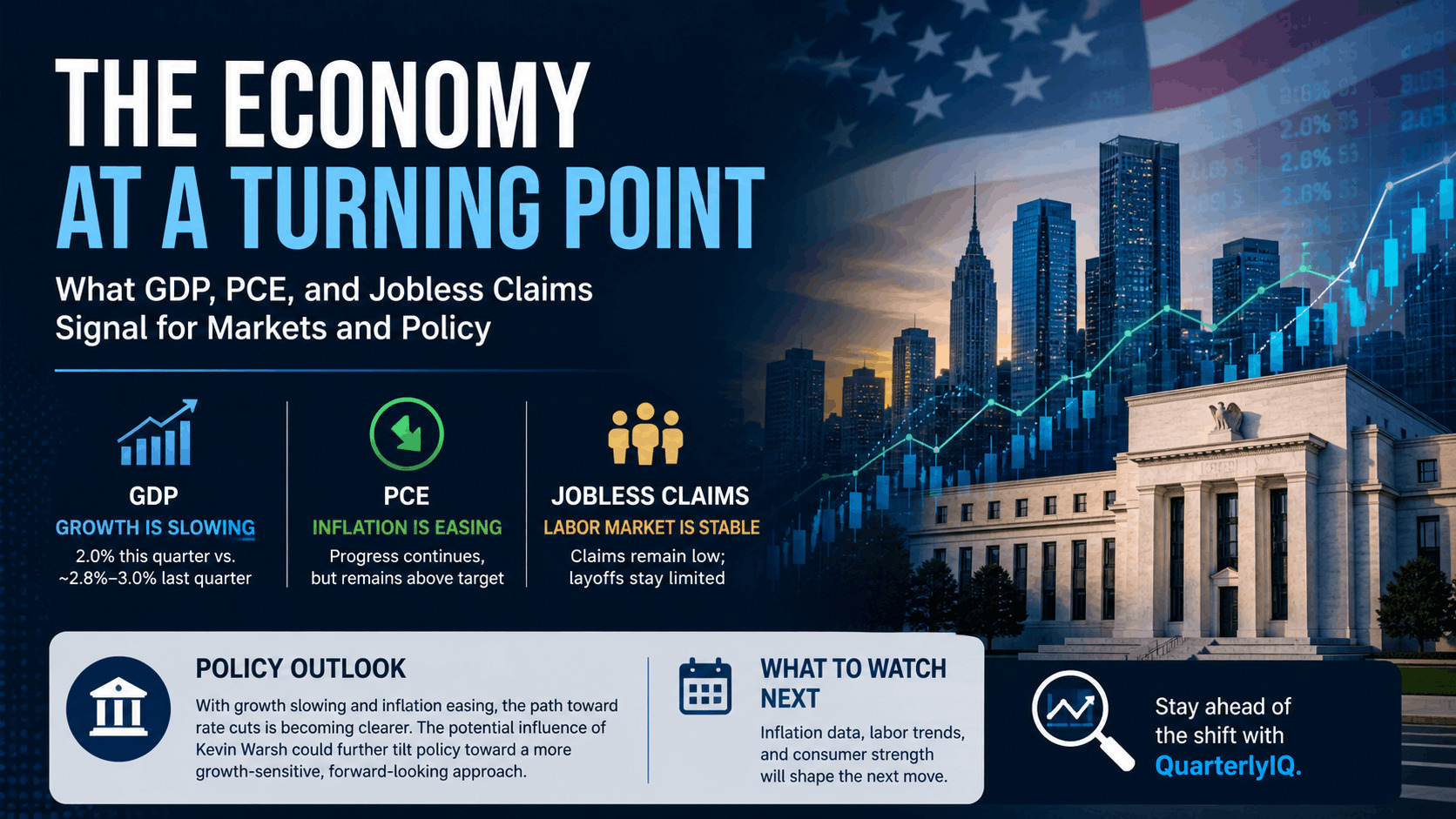

The latest GDP print came in around 2.0%, down from roughly 2.8% to 3.0% in the prior quarter.

That shift matters.

The level of growth is still healthy and close to the long-term trend. The change in direction is what investors should focus on.

Growth is no longer accelerating. It is cooling from a stronger pace.

QuarterlyIQ’s GDP framework emphasizes:

- Multi-quarter trend direction

- Momentum shifts rather than single prints

- Risk classification tied to changes in growth

The current signal is clear:

Growth is moderating, not breaking

This is a typical late-cycle pattern where momentum fades, but the expansion continues.

PCE: Inflation Is Cooling Gradually

PCE continues to move in the right direction, though progress remains gradual.

The data shows:

- Inflation is still above target

- Monthly readings are easing

- The broader trend is downward

QuarterlyIQ’s PCE models are designed to capture:

- Direction over noise

- Moderate risk levels rather than extremes

- Confidence ranges that reflect uncertainty

The takeaway remains consistent:

Inflation is easing, but not fully resolved

This keeps the Federal Reserve in a cautious position.

Jobless Claims: Labor Remains Stable

Jobless claims have not confirmed a weakening labor market. Recent readings suggest stability, and in some cases, slight improvement.

Claims remain low relative to historical levels and have not shown a sustained upward trend.

This indicates:

- Layoffs remain limited

- Labor demand is still intact

- The economy is not showing stress through employment

QuarterlyIQ’s labor signals are built to detect inflection points early. At this stage, the signal is:

Labor is stable, not weakening

This is an important distinction for policy expectations.

The Combined Signal: A Controlled Slowdown

When viewed together, the data presents a balanced picture:

- GDP is moderating

- Inflation is easing

- Labor remains stable

This is not a broad slowdown across all areas. It is a controlled cooling of the economy.

The expansion is still intact, but momentum is fading.

Policy Implications: Why Rate Cuts Are Getting Closer

The Federal Reserve is balancing two competing realities:

- Growth is slowing, and inflation is easing

- Labor remains stable and does not require immediate support

This creates a narrow policy path.

If labor begins to weaken, the case for rate cuts strengthens quickly. If labor remains stable, the Fed has room to wait.

At this stage, the data supports a gradual shift toward easing, but not urgency.

The Kevin Warsh Factor

The potential influence of Kevin Warsh adds an important dimension.

Warsh has historically emphasized:

- Responding to shifts in growth

- Taking a forward-looking approach to policy

- Monitoring financial conditions closely

In an environment where growth is moderating and inflation is easing, this perspective would likely support a more flexible stance over time.

However, with labor still stable, even a more growth-sensitive approach would likely favor patience in the near term.

The implication is not immediate rate cuts, but a growing probability that the next policy move will eventually be toward easing.

Market Implications: A Transition Environment

This macro setup leads to a different kind of market behavior.

1. Rate Expectations Are Shifting

Markets are beginning to price in future easing, but with limited conviction.

Each data release has an outsized impact on expectations.

2. Leadership Is Less Defined

With mixed macro signals:

- Growth sectors benefit from lower rate expectations

- Cyclicals face pressure from moderating growth

- Financials see mixed impacts

This results in more balanced market leadership.

3. Volatility Becomes Data-Driven

Without a dominant macro trend, markets respond more directly to new information.

This often leads to:

- Short-term swings

- Faster narrative changes

- Greater sensitivity to macro data

How Well Did QuarterlyIQ Call This?

QuarterlyIQ is built to identify changes in direction rather than predict exact numbers.

Based on the latest data:

- GDP moderation was captured through trend signals

- PCE cooling was reflected in inflation models

- Labor stability remained consistent with prior readings

This results in a coherent view:

The platform identified a slowing but stable economy before it became obvious in the data

What to Watch Next

The next phase depends on confirmation across three areas:

- Continued progress in inflation

- Stability or softening in labor conditions

- Evidence of slowing or resilient consumption

If labor begins to weaken, rate cuts become more likely. If labor remains stable, policy will likely move more slowly.

Final Thought

Macro transitions are rarely clean.

Right now, the data shows:

- Growth is moderating

- Inflation is easing

- Labor is holding

That combination creates a more complex environment where timing matters more than direction.

QuarterlyIQ is built to track these shifts as they develop, not after they become obvious.

This data does not signal a turning point yet.

It signals that we are getting closer to one.