High P/E Does Not Always Mean Overvalued

A high price-to-earnings ratio can make a stock look expensive at first glance.

It is easy to see a company trading at 40, 60, or 100 times earnings and assume the market has become too optimistic.

Sometimes that conclusion is right.

Other times, the P/E ratio is only the beginning of the analysis.

A stock can have a high P/E because investors are paying for durable growth, strong margins, recurring revenue, low capital needs, a high-quality business model, or temporarily depressed earnings that may recover.

A stock can also have a low P/E because earnings are about to decline, the business is cyclical, debt is high, competition is intensifying, or investors do not trust the durability of current profits.

The P/E ratio tells you how much investors are paying for each dollar of earnings.

It does not tell you whether those earnings are stable, growing, shrinking, temporarily distorted, or worth paying more for.

To understand whether a high P/E is reasonable or risky, you need to look at what the price already assumes and whether the business can realistically deliver.

What the P/E ratio actually measures

The P/E ratio compares a company’s stock price with its earnings per share.

A simple version looks like this:

P/E ratio = stock price divided by earnings per share

If a stock trades at $100 and the company earns $5 per share, the P/E ratio is 20.

That means investors are paying 20 times the company’s current or expected earnings, depending on whether the ratio uses past earnings or future estimates.

There are two common versions:

Trailing P/E

Trailing P/E uses earnings from the past 12 months.

It shows how the current price compares with earnings the company has already reported.

This can be useful, but it may be misleading when earnings are unusually high or unusually low.

Forward P/E

Forward P/E uses estimated earnings for a future period.

It attempts to compare the current price with what analysts expect the company to earn next.

This can be more relevant for forward-looking investors, but it depends on estimates that may change.

Both versions can be useful.

Neither version is complete on its own.

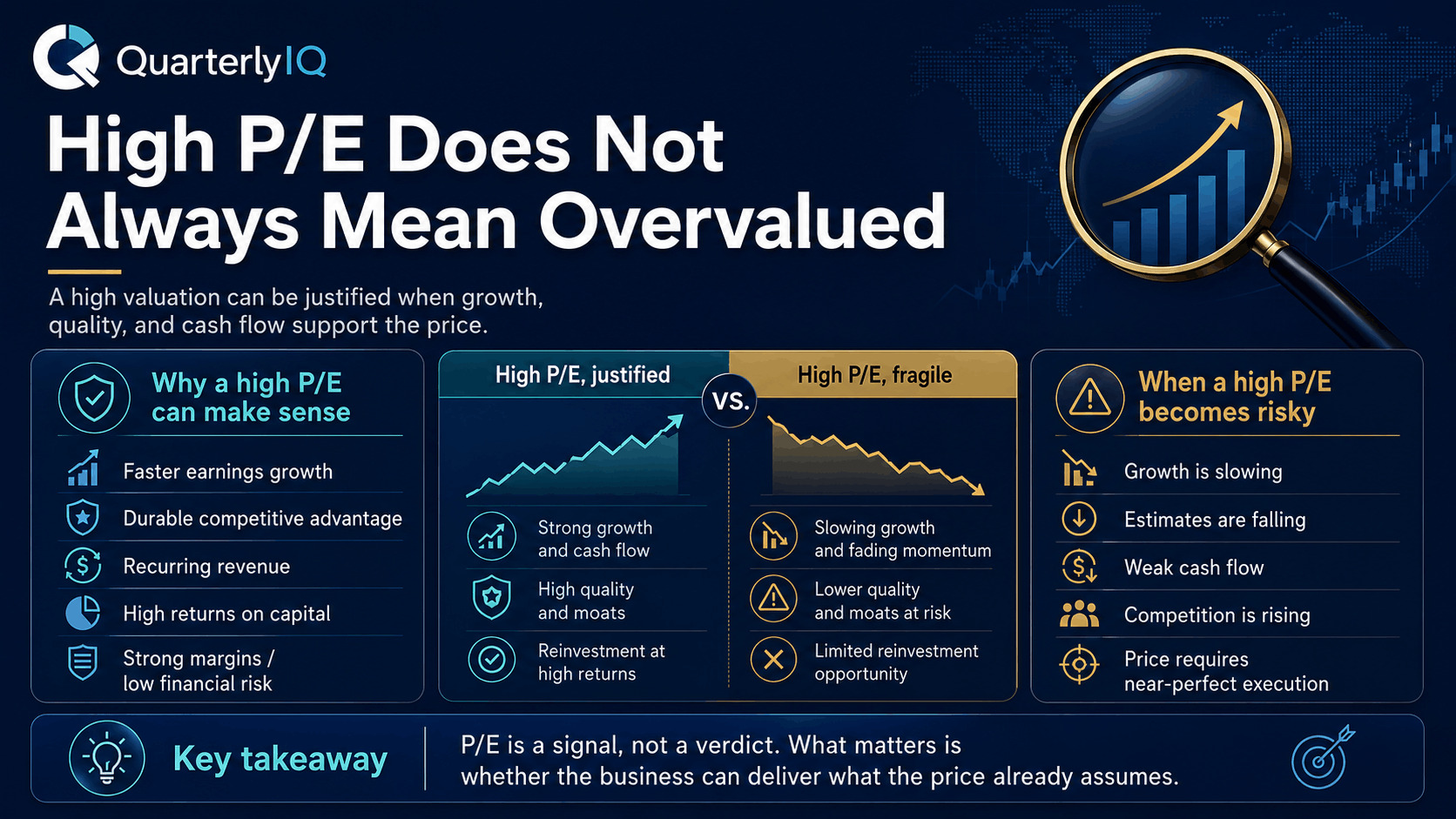

Why a high P/E can be justified

A high P/E usually means investors expect more from the company.

That expectation may be reasonable when the business has strong characteristics.

Faster earnings growth

If a company can grow earnings quickly for many years, investors may be willing to pay a higher multiple today.

A company earning $1 per share today may look expensive at 50 times earnings.

But if earnings grow to $5 per share over time, the valuation may look very different.

The key question is not whether the current P/E is high.

The question is whether future earnings can grow enough to support the price.

Durable competitive advantages

Some businesses can defend their profits better than others.

A company with strong switching costs, network effects, trusted brands, cost advantages, or proprietary technology may deserve a higher valuation than a business whose profits are easier to copy.

Investors may pay more because they believe the company’s earnings are more durable.

High returns on capital

A company that can reinvest money at high returns may create more value from each dollar of profit.

That matters because two companies with the same earnings can have very different futures.

One may need heavy capital spending simply to maintain its current position.

Another may be able to grow with limited additional investment.

The second business may deserve a higher P/E because its earnings can compound more efficiently.

Recurring or predictable revenue

Companies with recurring revenue, strong retention, and predictable demand often receive higher valuations.

Investors may value those earnings more because they appear less uncertain.

A dollar of earnings that is likely to repeat next year may be worth more than a dollar of earnings that depends on a one-time event or a favorable commodity cycle.

Strong margins and operating leverage

Some companies become much more profitable as they grow.

Revenue may increase faster than costs, allowing margins to expand over time.

If investors believe a company is still early in that margin expansion, they may accept a high current P/E because they expect future earnings to rise faster than revenue.

Lower financial risk

A business with a strong balance sheet, reliable cash flow, and modest debt may deserve a higher multiple than a more fragile company.

Lower financial risk can make future earnings more valuable.

Investors may be willing to pay more when the company has flexibility to invest, endure downturns, and avoid diluting shareholders.

A high P/E can also be a warning sign

A high P/E is not automatically bad, but it does show that expectations may be demanding.

The higher the valuation, the more important the company’s future delivery becomes.

A high P/E may be risky when:

- Growth is already slowing

- Margins are peaking

- Earnings quality is weak

- Competition is increasing

- The company depends on a narrow product or customer base

- Estimates are being revised lower

- Interest rates make future earnings less valuable

- The business needs near-perfect execution to justify the price

A high P/E becomes more concerning when the business evidence no longer supports the expectations embedded in the price.

The risk is not simply that the multiple is high.

The risk is that the company may not deliver what the multiple requires.

The same P/E can mean different things for different companies

A 40 times earnings multiple does not mean the same thing for every business.

For one company, it may be too high.

For another, it may be reasonable.

For a third, it may even be too low if earnings are early in a long growth cycle.

The difference depends on the business.

Consider the factors that affect how much a dollar of earnings may be worth:

- How fast earnings can grow

- How long growth can continue

- How predictable revenue is

- How durable the company’s advantage is

- How much capital the company needs

- How cyclical the business is

- How much debt the company carries

- How much confidence investors have in management

- How much uncertainty surrounds the future

P/E is a comparison tool.

It is not a verdict.

A low P/E does not automatically mean cheap

Many investors make the opposite mistake too.

They see a low P/E and assume the stock is undervalued.

That can be dangerous.

A low P/E may reflect real concern about the business.

The company may be cheap because investors expect:

- Earnings to decline

- Margins to compress

- Competition to intensify

- Debt to become a problem

- Demand to weaken

- A favorable cycle to reverse

- Management to allocate capital poorly

- Cash flow to be weaker than reported earnings

A stock trading at 8 times earnings may look inexpensive.

But if earnings fall by half, the effective valuation was not as cheap as it appeared.

Low multiples often come with a reason.

The job is to determine whether that reason is temporary, exaggerated, or justified.

Cyclical companies can make P/E ratios misleading

P/E ratios can be especially tricky for cyclical businesses.

These companies may experience large swings in earnings because demand, pricing, or input costs move with the economic cycle.

Examples may include industries tied to commodities, housing, manufacturing, travel, autos, or financial conditions.

A cyclical company can look cheapest near peak earnings.

When profits are unusually high, the P/E may appear low.

But if those earnings are not sustainable, the low ratio can be misleading.

The reverse can also happen.

A cyclical company can look expensive when earnings are temporarily depressed.

If profits are near a trough, the P/E may appear high or even meaningless.

In these cases, investors often need to evaluate normalized earnings rather than one unusually strong or weak year.

The central question is:

Are current earnings a reasonable picture of the business, or are they unusually high or low?

Fast-growing companies can look expensive before they look reasonable

Some companies look expensive for years while the business grows into its valuation.

This does not mean every high-growth stock is attractive.

It means a high P/E must be evaluated against the company’s future earnings potential.

A young company may be investing heavily in sales, research, infrastructure, or product development.

Those investments can reduce current earnings.

If they lead to much larger earnings later, the current P/E may overstate how expensive the business really is.

But this requires evidence.

Investors should ask:

- Is revenue growing quickly enough?

- Are customers staying and spending more?

- Is the company gaining market share?

- Are margins improving or likely to improve?

- Does the business model produce cash as it scales?

- Are estimates rising or falling?

- Is management delivering on earlier goals?

A high-growth story becomes fragile when growth slows before profitability improves.

Accounting can distort the P/E ratio

Earnings are an accounting measure.

They can be affected by items that do not fully reflect the underlying health of the business.

A company’s P/E may look unusually high or low because of:

- One-time gains or losses

- Restructuring charges

- Acquisition-related costs

- Asset impairments

- Tax effects

- Stock-based compensation

- Changes in depreciation or amortization

- Litigation expenses

- Currency movements

This does not mean earnings should be ignored.

It means investors should understand what is inside the earnings number.

A high P/E based on temporarily depressed earnings may not be as expensive as it looks.

A low P/E based on temporarily inflated earnings may not be as cheap as it looks.

Cash flow, margins, and earnings quality can help clarify the picture.

Growth must eventually become earnings or cash flow

A high P/E often depends on the belief that earnings will grow.

That makes the quality of growth extremely important.

Revenue growth alone is not enough.

A company may grow sales while failing to produce durable profits or cash flow.

Investors should ask:

- Is growth becoming more profitable over time?

- Are margins improving as the company scales?

- Is customer acquisition becoming more efficient?

- Is free cash flow improving?

- Does the company need constant capital raises?

- Are existing customers expanding their spending?

- Is growth coming from sustainable demand or heavy discounting?

A high P/E can be more reasonable when growth is paired with improving economics.

It becomes more dangerous when growth requires increasing amounts of spending without evidence of future profitability.

The P/E ratio depends on interest rates

Valuation is also influenced by the broader market environment.

When interest rates are low, investors may be willing to pay more for future earnings because alternative returns are less attractive.

When interest rates rise, future earnings may become less valuable in today’s terms, especially for companies expected to earn most of their profits far in the future.

This can pressure high-P/E stocks even when the business itself continues performing well.

The company may not have weakened.

Investors may simply be less willing to pay the same multiple for future growth.

This is one reason valuation should not be reviewed in isolation from the market environment.

A high P/E may be easier to support when rates are low, growth is scarce, and earnings visibility is high.

It may become harder to support when rates rise, uncertainty increases, or investors demand a larger margin of safety.

Sector comparisons matter

P/E ratios are more useful when compared with similar companies.

A software company, bank, utility, retailer, and industrial manufacturer may naturally trade at very different valuations.

Those differences can reflect:

- Growth expectations

- Margin structure

- Capital intensity

- Regulation

- Cyclicality

- Balance-sheet risk

- Revenue predictability

- Competitive dynamics

Comparing a high-growth software company with a slow-growth utility may not tell you much.

Comparing two companies with similar business models can be more useful.

Even then, the higher-P/E company may deserve the premium if it has better growth, stronger margins, lower risk, or more durable competitive advantages.

The question is whether the premium is supported by the evidence.

The market may be pricing in a long runway

Some companies receive high valuations because investors believe they have a long runway for growth.

A long runway may come from:

- A large addressable market

- Low current penetration

- New product categories

- International expansion

- Increased customer spending

- Industry digitization

- A shift from legacy providers

- A scalable business model

A long runway can justify a higher valuation only if the company has a credible path to capture it.

A large market opportunity is not enough.

Many companies operate in large markets without producing attractive shareholder returns.

Investors should look for evidence that the company is converting the opportunity into durable results.

That evidence may include customer growth, market-share gains, pricing power, retention, margin progress, and cash generation.

A high P/E means expectations are already part of the price

This is where the idea of being “priced in” matters.

A high P/E often means investors are already paying for strong future performance.

That does not make the stock overvalued by itself.

It does mean the company may need to deliver a lot to justify the current price.

Ask:

- What growth rate does the valuation appear to require?

- How long does growth need to continue?

- Do margins need to expand?

- Does the company need to gain market share?

- Are estimates rising enough to support the price?

- How much disappointment can the stock absorb?

- What would cause investors to reduce the multiple?

A stock with a high P/E can continue performing well if the company keeps exceeding expectations.

It can struggle if the company merely performs well but not well enough.

For more on this idea, read What Does “Priced In” Mean in the Stock Market?.

Estimate revisions can change the meaning of a P/E ratio

A P/E ratio is not static.

It changes as price changes and earnings estimates change.

A stock may appear expensive based on current earnings, but the forward P/E may decline if analysts expect earnings to grow significantly.

A stock may appear reasonably valued today, but it can become more expensive if estimates are revised lower while the price remains high.

Watch the direction of:

- Revenue estimates

- Earnings estimates

- Margin forecasts

- Free cash flow estimates

- Long-term growth assumptions

A rising P/E with rising estimates may reflect improving confidence.

A rising P/E with flat estimates may reflect multiple expansion.

A high P/E with falling estimates may signal increasing valuation risk.

The relationship between price and estimates often matters more than the P/E number alone.

Quality can deserve a premium, but not unlimited optimism

High-quality companies often deserve higher valuations.

They may have stronger margins, better returns on capital, more predictable revenue, stronger balance sheets, and more credible management teams.

But quality does not remove valuation risk.

A great business can still become a fragile investment if the stock price assumes too much.

The more optimistic the valuation becomes, the more sensitive the stock may be to:

- Slower growth

- Margin pressure

- Missed guidance

- Estimate cuts

- Competitive threats

- Higher interest rates

- A change in investor sentiment

Quality can justify a premium.

It cannot justify every price.

The central question is whether the quality of the business is strong enough to support the expectations embedded in the valuation.

When a high P/E may be reasonable

A high P/E may be more reasonable when several conditions are present:

- Revenue is growing consistently

- Earnings are expected to grow faster than the market

- Margins have room to expand

- The company has a durable competitive advantage

- Customer retention is strong

- Cash flow is improving

- Returns on capital are attractive

- Debt is manageable

- Management has a record of execution

- Estimates are stable or rising

- The valuation premium is supported by business quality

The stronger the evidence, the easier it is to understand why investors might pay more.

The P/E may still be high.

The question is whether the business can grow into it.

When a high P/E may be dangerous

A high P/E deserves more caution when:

- Growth is slowing

- Margins are already near peak levels

- Earnings estimates are being reduced

- Cash flow is weak

- The company depends on one product or customer

- Competition is intensifying

- Management credibility is declining

- The balance sheet is stretched

- The valuation requires flawless execution

- Investor enthusiasm is based more on narrative than evidence

In these situations, a high P/E can become fragile.

The stock may not need terrible news to fall.

It may only need results that are slightly less impressive than investors expected.

Use a practical high-P/E checklist

When reviewing a stock with a high P/E, work through these questions.

1. Which P/E are you looking at?

Is the ratio based on trailing earnings or forward estimates?

Are earnings temporarily high or low?

2. Why is the multiple high?

Is the market paying for growth, margins, quality, predictability, a recovery, or a temporary accounting distortion?

3. What does the company need to deliver?

Identify the revenue growth, earnings growth, margin expansion, or cash flow improvement required to justify the price.

4. Is the evidence supporting that path?

Review growth quality, customer behavior, competitive strength, management execution, and estimate revisions.

5. How much room is there for disappointment?

A high valuation may leave little room for delays, missed guidance, or weaker margins.

6. How does the company compare with peers?

Is the premium supported by better growth, profitability, cash flow, or lower risk?

7. Are estimates moving higher or lower?

A high P/E becomes more concerning when future expectations are being revised down.

8. Is the business becoming stronger or just more popular?

Market enthusiasm can push a valuation higher even when business evidence has not improved.

9. What would cause the thesis to weaken?

Define the conditions that would make the valuation harder to defend.

10. Would you still find the risk and reward attractive today?

A stock may have been reasonable at one price and fragile at another.

The review should focus on the current evidence, not only the original purchase decision.

Avoid using P/E as a shortcut

The P/E ratio is useful because it is simple.

That simplicity is also its weakness.

It can help start the conversation, but it should not end it.

A high P/E does not automatically mean overvalued.

A low P/E does not automatically mean undervalued.

The right question is not whether the multiple is high or low in isolation.

The right question is whether the company can deliver the growth, profitability, cash flow, and durability that the current price appears to require.

How this connects to an investment thesis

A valuation is only meaningful when connected to a thesis.

If your thesis is that a company can grow earnings rapidly for many years, a high P/E may be part of the setup.

If your thesis is that a company is mature, slow-growing, and only modestly profitable, the same P/E may be difficult to justify.

The P/E ratio should be reviewed alongside:

- The original reason for owning the stock

- The expected business drivers

- The evidence supporting those drivers

- The risks that could challenge the thesis

- The valuation assumptions already reflected in the price

For a broader framework, read How to Tell if a Stock Is Overvalued Without One Magic Ratio.

Monitoring a high-P/E stock after you buy

High-P/E stocks often require more careful monitoring because expectations are already elevated.

After buying, watch whether the company continues to support the assumptions behind the valuation.

Monitor:

- Revenue growth

- Margin expansion

- Cash flow improvement

- Customer retention

- Competitive position

- Management guidance

- Estimate revisions

- Valuation relative to growth

- Changes in interest rates

- Signs that the thesis is becoming more fragile

A high-P/E stock does not need to be watched because it is automatically wrong.

It needs to be watched because the price may already assume a lot of success.

For more on monitoring after the purchase, read How to Monitor a Stock After You Buy It.

Why this becomes difficult across a portfolio

It is hard enough to evaluate the P/E ratio of one company properly.

It becomes much harder across a portfolio.

Each holding may have a different reason for its valuation.

One company may trade at a high P/E because of rapid growth.

Another may trade at a low P/E because earnings are near a cyclical peak.

A third may have temporarily depressed earnings.

A fourth may be priced for margin recovery.

A fifth may deserve a premium because of quality and predictability.

A portfolio review should not simply sort holdings from highest P/E to lowest P/E.

It should ask whether each valuation is supported by the company’s thesis, business evidence, and expectations.

How QuarterlyIQ approaches valuation

QuarterlyIQ helps investors look beyond simple valuation shortcuts.

For covered companies, we focus on practical questions:

- What does the current valuation appear to assume?

- Is the company delivering enough to support those assumptions?

- Are estimates moving higher or lower?

- Is the valuation becoming more or less demanding?

- Does the business quality justify a premium?

- How much room appears to remain for disappointment?

- What should be watched next?

The goal is not to label a stock as cheap or expensive based on one ratio.

It is to connect valuation with the business evidence and the investment thesis.

Explore the QuarterlyIQ stock research section to review covered companies.

The takeaway

A high P/E ratio is a signal, not a conclusion.

It may indicate that investors expect rapid growth, durable profits, strong margins, predictable revenue, or unusually high business quality.

It may also indicate that the stock has little room for disappointment.

The difference depends on the evidence.

Before deciding that a high-P/E stock is overvalued, ask what the business needs to deliver, whether that path is realistic, and whether the current price already assumes too much.

A stock is not overvalued simply because the P/E is high.

It becomes overvalued when the expectations embedded in the price are greater than the business is likely to deliver.

For a deeper look at expectations and valuation, read What Does “Priced In” Mean in the Stock Market?.

For a broader valuation framework, read How to Tell if a Stock Is Overvalued Without One Magic Ratio.

For informational purposes only. Not investment advice. QuarterlyIQ provides descriptive, rules-based analysis of company fundamentals and does not recommend buying or selling any security.