Expectations 101: Before Earnings, Watch the Bar, Not the Beat

A company can beat earnings and still see its stock fall. The reason is simple: by earnings day, the market is usually grading results against expectations, not just the headline numbers.

A company can beat earnings and still see its stock fall. That sounds backward, but it happens all the time.

This week gave investors two good examples. Goldman Sachs reported first-quarter 2026 revenue of $17.23 billion and diluted earnings per share of $17.55. 3M reported adjusted EPS of $2.14 on adjusted sales of $6.0 billion and kept its full-year 2026 guidance in place. On the surface, those both look like solid reports. But both stocks still slipped after earnings, because investors were focused on what came next and what still looked weak. Goldman’s fixed-income, currency, and commodities revenue fell 10%, while 3M warned that higher oil prices could add about $125 million in annual costs.

That is the real lesson of earnings season. Stocks do not move only on whether a company beat or missed. They move on the gap between what investors expected and what the company actually delivered. The setup matters as much as the score. Sometimes more.

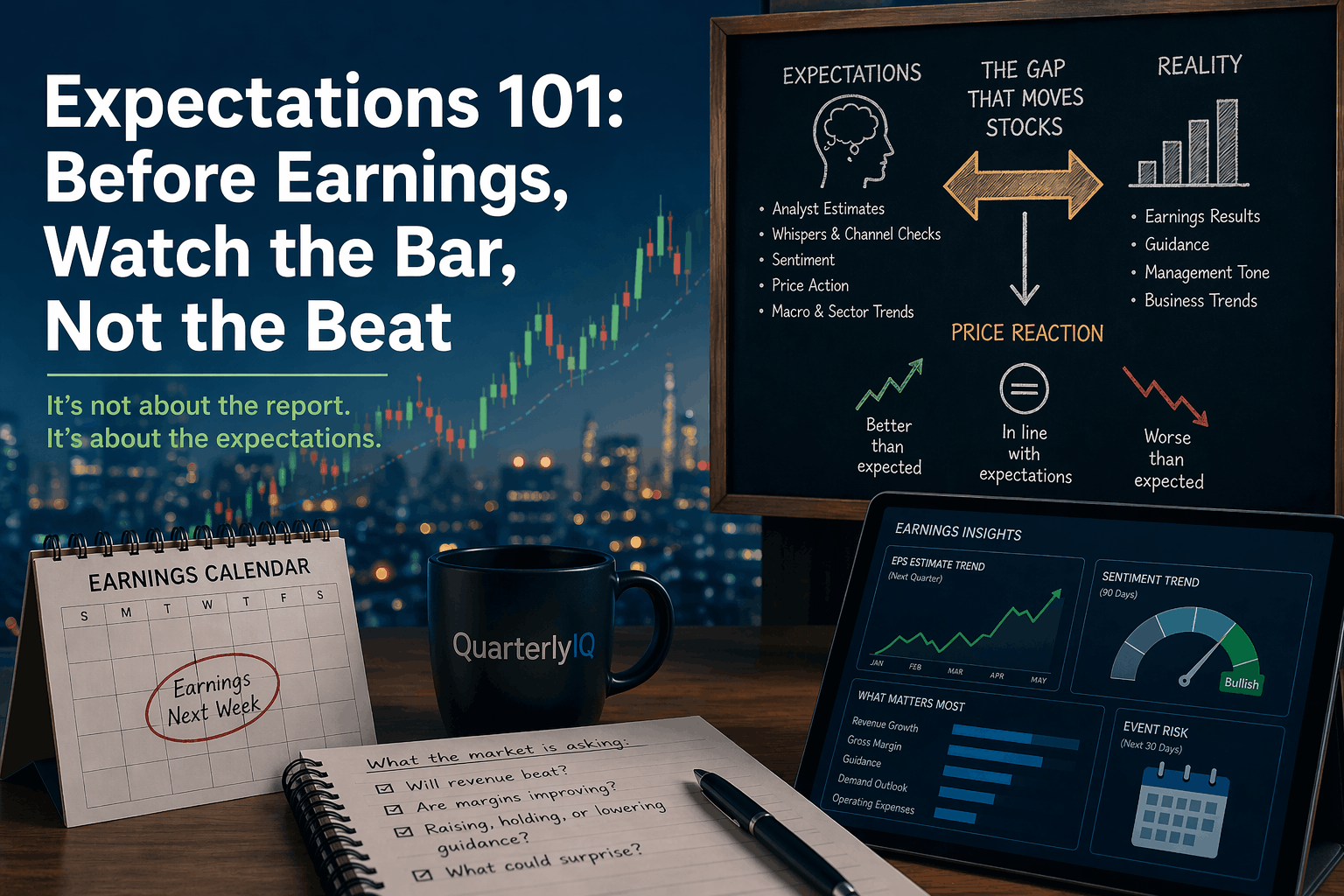

The market sets the bar before the report

Most people treat earnings like the big reveal. In reality, the market starts reacting long before the press release shows up.

Analysts revise estimates. Investors build a story in their heads. Traders watch peers, margins, and macro signals and start placing bets. By the time earnings day arrives, the stock has often already moved on those expectations.

This quarter, the bar was rising in several parts of the market. FactSet said total estimated S&P 500 earnings for Q1 2026 had increased by 0.4% since December 31, to $629.3 billion from $627.0 billion. It also said more companies issued positive EPS guidance than negative guidance, 59 to 51. Most of that upside came from Information Technology and Energy, with Financials also showing a small increase. That means some sectors did not walk into earnings season with low expectations. They walked in with a tougher audience.

Why a beat can still disappoint

Goldman is a clean example of how this works.

The bank’s headline numbers were strong. Revenue rose to $17.23 billion, net earnings reached $5.63 billion, and investment banking fees were up sharply from a year earlier. But the market did not grade Goldman on the headline alone. Investors also focused on the softer part of the story, especially the drop in fixed-income trading. Reuters reported that Goldman shares fell 1.9% after the results. In other words, Goldman did not fail the quarter. It just did not clear every part of the bar investors had quietly built ahead of time.

3M told a similar story from a very different sector. The company beat profit expectations, posted adjusted EPS up 14% year over year, and improved adjusted operating margin by 30 basis points. But it also repeated, rather than raised, its full-year guidance, and flagged higher oil prices as a cost risk. Reuters said the stock fell more than 1% in morning trading after the report. The market heard the beat, then looked straight past it to costs, margins, and the second half of the year.

That is why “beat” and “miss” are often too shallow to be useful. A company can beat and still disappoint if the outlook cools, margins soften, or investors were hoping for more. A company can miss and still rise if expectations were already low and the report shows the worst may be over. The number matters. The setup tells you how much it matters.

What this means for sectors and stocks

This gets even more important when you zoom out from one company to a whole sector.

If expectations are rising across a sector, companies may need more than decent results to keep stocks moving higher. They may need stronger guidance, better margins, or proof that demand is holding up. FactSet’s preview suggests Technology, Energy, and to a lesser degree Financials entered Q1 earnings season with a higher bar than usual because earnings expectations had already moved up.

That does not mean those sectors are bad places to look. It means the market may be less forgiving there. A solid quarter in a low-expectation sector can sometimes do more for a stock than a strong quarter in a high-expectation one.

Same earnings season. Different starting line.

What to watch before the next report

Before the next wave of earnings, the smarter questions are not just, “Will this company beat?”

They are:

Is the market already expecting a lot? Have analyst estimates been moving up or down? What are competitors saying about demand, pricing, and margins? Is the macro backdrop helping or hurting the business?

Those questions usually tell you more than the final headline number.

Bottom line

Before earnings, do not just watch the beat. Watch the bar.

That is where the real signal usually hides. By the time the report lands, the market has often already decided what good was supposed to look like. The stock then moves on whether reality was better, worse, or just a little too ordinary.

That is the setup investors need to watch.