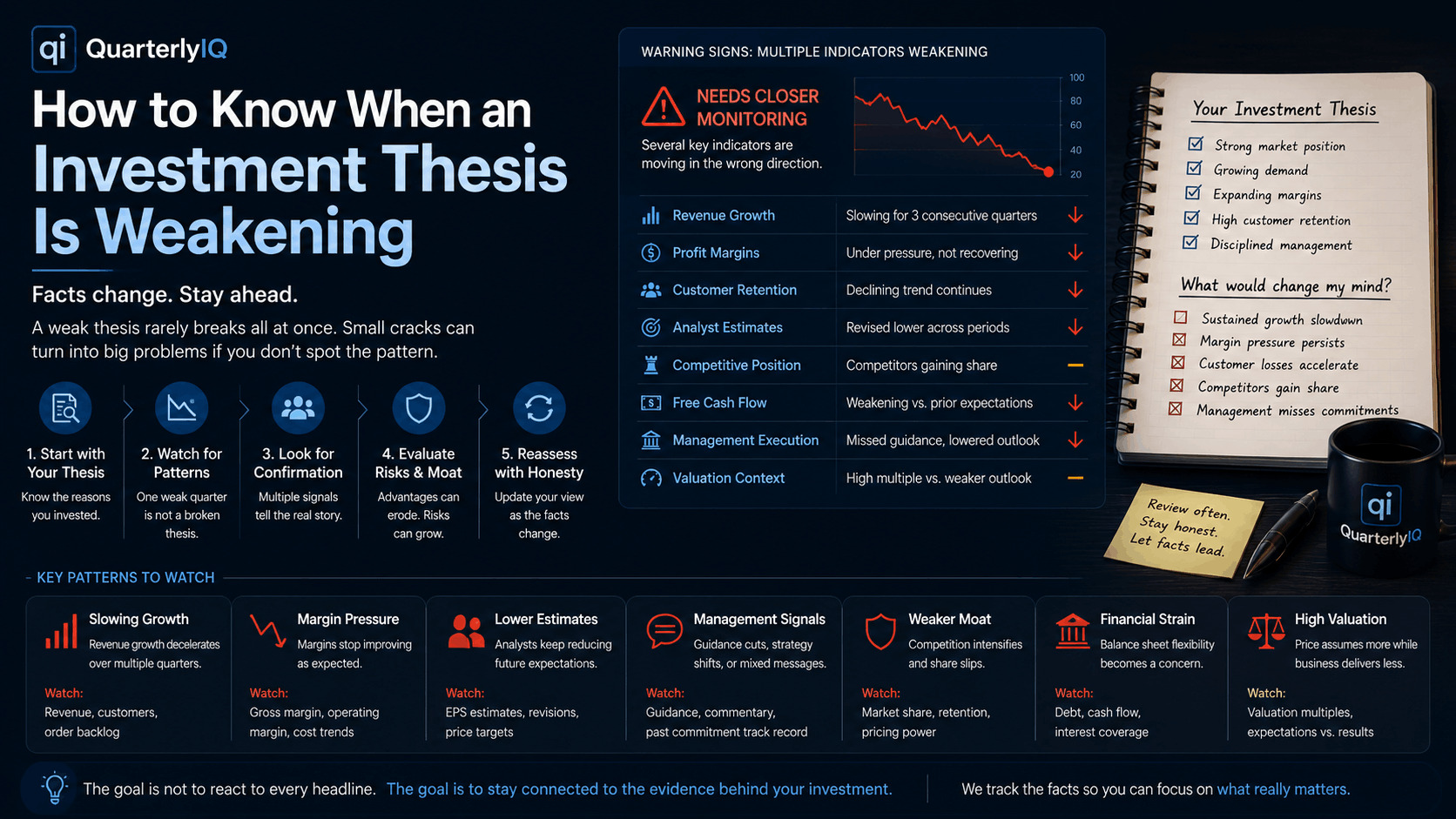

How to Know When an Investment Thesis Is Weakening

An investment thesis rarely falls apart in one dramatic moment.

More often, it weakens quietly.

Growth slows a little. Margins stop improving. Management explains away a disappointing quarter. Analysts trim their estimates. A competitor begins gaining ground.

Each development may look manageable on its own.

When several of them begin pointing in the same direction, the investment may no longer be developing the way you originally expected.

Recognizing that change is one of the most difficult parts of investing. It requires patience, honesty, and a willingness to separate temporary setbacks from evidence that the business itself is moving in a less favorable direction.

Start with the original reason you owned the company

You cannot tell whether a thesis is weakening unless you know what the thesis was.

A useful investment thesis explains:

- What the company does especially well

- What is expected to drive future growth or profitability

- What evidence supports that view

- Which risks matter most

- What developments would cause you to reconsider the original reasoning

Imagine that your thesis depends on a company continuing to grow revenue, expand margins, and retain customers because its product is difficult to replace.

The thesis should be reviewed when those specific conditions begin changing.

A falling share price alone does not prove that the thesis has weakened. A rising price does not prove that the thesis remains healthy.

The business evidence is what allows you to tell the difference.

A weak quarter is not always a weak thesis

Every business has uneven periods.

Demand may shift between quarters. Costs may rise temporarily. A product launch may be delayed. Foreign exchange rates may affect reported results. Customers may postpone purchases without abandoning them.

One disappointing quarter deserves attention, but it rarely tells the entire story.

The surrounding context matters:

- Was the weakness expected?

- Did management explain it clearly?

- Is the problem temporary or continuing?

- Are competitors experiencing the same conditions?

- Did the company maintain its longer-term guidance?

- Are customers still buying, renewing, and expanding?

- Is cash flow holding up?

- Are analysts treating the issue as temporary or revising future expectations?

A temporary setback affects the current period.

A weakening thesis affects the assumptions behind the future.

Look for persistence, not perfection

A healthy thesis does not require every metric to improve every quarter.

What matters is whether the company remains broadly on the path you expected.

A warning sign becomes more meaningful when it persists.

For example:

- Revenue growth slows for several quarters rather than one

- Margins remain under pressure after temporary costs should have passed

- Customer retention continues declining

- Management repeatedly lowers expectations

- Analysts continue reducing estimates

- Competitive losses become more frequent

- Cash generation fails to improve despite reported earnings growth

Persistence turns an isolated concern into a pattern.

The goal is not to react to the first negative data point. It is to notice when the explanation for each new disappointment begins sounding like the explanation for the last one.

Watch for several signals confirming one another

One weak metric can mislead you.

Several related metrics moving together deserve more attention.

Suppose revenue growth slows. That may not be alarming on its own.

Now add:

- Lower customer growth

- Smaller order sizes

- Reduced guidance

- Falling analyst estimates

- Rising sales incentives

- Weaker margins

The combined picture is more meaningful than any single number.

This is sometimes called confirmation or triangulation. You are looking for evidence from different parts of the business that supports the same conclusion.

Useful combinations include:

Slower growth and lower estimates

A slowing company may still have a healthy thesis if the slowdown is modest and expected.

The concern grows when analysts repeatedly reduce future revenue or earnings estimates at the same time.

Margin pressure and weak cash flow

Margins can fall because a company is investing for growth.

That explanation becomes less convincing when cash flow also weakens and the promised growth does not appear.

Customer losses and competitive pressure

One lost customer may not matter.

A pattern of lost customers, weaker retention, and stronger competitors may challenge the company’s core advantage.

Lower guidance and missed commitments

Management may lower guidance for sensible reasons.

Repeated reductions, especially after confident promises, can weaken confidence in both the outlook and the leadership team.

Revenue growth begins to lose quality

Slower revenue growth is one of the most visible signs of potential thesis weakness, but the headline rate is only part of the story.

Look underneath it.

Ask:

- Is growth coming from more customers or higher prices?

- Are existing customers buying more?

- Is the company relying heavily on one product?

- Is growth being purchased through discounts?

- Are sales incentives increasing?

- Is deferred revenue or backlog supporting future demand?

- Is organic growth weaker than reported growth?

- Are acquisitions hiding weakness in the core business?

A company may continue reporting growth while the quality of that growth deteriorates.

For example, revenue may rise because prices increased even though customer volume fell. That can work for a while, but it may become difficult to repeat.

Margins stop developing as expected

Many investment theses depend on a company becoming more profitable as it grows.

The expectation may be that fixed costs spread across a larger revenue base, manufacturing becomes more efficient, or customer acquisition becomes less expensive.

When those improvements fail to appear, the thesis may need another look.

Margin pressure deserves attention when:

- It persists beyond the period management originally described

- Costs grow faster than revenue

- Discounts become necessary to support sales

- Product mix shifts toward less profitable offerings

- Input costs rise without corresponding pricing power

- Management stops discussing prior margin goals

- Adjusted earnings improve while cash generation does not

The concern is not simply that margins fell.

It is that the business may no longer have the operating leverage or pricing power assumed in the original thesis.

Earnings estimates keep moving lower

Analyst estimates are not perfect, but the direction of revisions can reveal how expectations are changing.

A single estimate reduction may reflect a temporary issue.

Repeated reductions across several months or quarters can indicate that the company’s outlook is becoming more difficult to defend.

Pay attention to:

- Revenue estimates

- Earnings estimates

- Margin expectations

- Free cash flow forecasts

- Price targets

- The number of analysts revising higher versus lower

- Changes across more than one forecast period

Estimate revisions are especially useful when they confirm what is already visible in company results.

They should not replace your own analysis. They can help show whether the broader evidence is improving or deteriorating.

Management’s words and actions begin to separate

Management credibility is an important part of many investment theses.

Executives cannot control every business condition. They can control how clearly they communicate, how they allocate capital, and whether they follow through on commitments.

Warning signs may include:

- Repeatedly missing guidance

- Changing the definition of key performance metrics

- Emphasizing adjusted results while cash flow weakens

- Avoiding questions about known problems

- Introducing new long-term goals before explaining missed ones

- Making acquisitions that conflict with the stated strategy

- Increasing share-based compensation without matching shareholder value creation

- Blaming external conditions that competitors are managing more effectively

No management team communicates perfectly.

The issue becomes more important when the company’s explanation changes more often than its performance improves.

The company’s competitive advantage begins to erode

A thesis often rests on the belief that the company has an advantage competitors cannot easily copy.

That advantage may come from technology, cost, brand, distribution, customer relationships, data, regulation, or network effects.

Competitive strength can weaken slowly.

Look for evidence such as:

- Falling market share

- Lower customer retention

- More aggressive discounting

- Competitors matching important product features

- Customers adopting alternative solutions

- Longer sales cycles

- Higher customer acquisition costs

- Reduced pricing power

- Key employees or partners leaving

- New technologies making the company’s offering less essential

Competition is always present.

The thesis becomes more vulnerable when the company must spend more, charge less, or promise more simply to maintain its existing position.

The balance sheet becomes part of the problem

A company can survive temporary operating weakness more easily when it has cash, manageable debt, and reliable cash generation.

Financial flexibility becomes more important when conditions become difficult.

A weakening balance sheet may show up through:

- Rising debt

- Falling cash reserves

- Higher interest costs

- Continued negative free cash flow

- Frequent share issuance

- Debt maturities approaching without a clear refinancing plan

- Acquisitions funded with increasingly expensive capital

- Dividends or repurchases that are not supported by cash generation

A thesis built around long-term growth may become harder to sustain when the company must focus on short-term financing.

The underlying opportunity may still exist, but shareholders may experience dilution or reduced strategic flexibility before the company reaches it.

The valuation assumes more while the business delivers less

A company’s fundamentals can weaken while its valuation remains demanding.

That creates a different kind of risk.

Suppose growth slows, estimates fall, and margins remain under pressure, but the stock continues trading at a premium because investors remain confident in the long-term story.

The price may then depend on fewer things going wrong.

Ask:

- Is the valuation rising or remaining high while estimates fall?

- Does the current price still assume rapid growth?

- Has the company’s execution become less reliable?

- Are investors paying for improvements that have not appeared?

- Is the valuation supported by current results or distant possibilities?

A strong business can carry a high valuation.

A weakening business with a high valuation has less room for disappointment.

The original thesis begins changing after every quarter

One of the clearest behavioral warning signs comes from the investor, not the company.

You may notice that you keep rewriting the thesis to preserve the conclusion.

The company misses a target, so the target becomes less important.

Growth slows, so the story shifts to margins.

Margins weaken, so the story shifts to market share.

Market share falls, so the story shifts to a future product.

The thesis has now become a moving target.

Updating a thesis as new information arrives is sensible. Replacing every failed assumption with a new one is different.

A helpful question is:

If I did not already own this stock, would the current evidence lead me to write the same thesis today?

That can reveal whether you are evaluating the company as it is or defending the decision you already made.

Separate company-specific weakness from broad market conditions

Not every decline in results or share price is unique to the company.

Interest rates, inflation, economic slowdowns, supply shortages, currency movements, and industry cycles can affect many businesses at once.

Compare the company with:

- Direct competitors

- Its sector

- Similar-sized businesses

- Companies exposed to the same customers

- The assumptions management made before conditions changed

If the entire industry is slowing, the company may still be performing relatively well.

If competitors are growing while the company is shrinking, the concern is more likely to be company-specific.

Broad conditions provide context. They do not automatically excuse poor execution.

A practical thesis review framework

When something concerning happens, work through the following steps.

1. Return to the written thesis

Identify which assumption the new information affects.

Does it challenge growth, margins, competitive strength, management execution, valuation, or financial stability?

2. Determine whether the change is isolated

Look for evidence across several quarters, metrics, and sources.

One data point may be noise. A repeated pattern deserves more attention.

3. Compare expectations with delivery

Review what management and analysts previously expected.

Did the company fall short once, or is the expected path being revised repeatedly?

4. Look for confirming evidence

Check whether customers, margins, cash flow, guidance, estimates, and competitive data are telling a similar story.

5. Consider the company’s response

Has management identified the problem, explained it clearly, and taken credible action?

6. Review valuation and financial flexibility

Determine whether the stock price and balance sheet leave room for recovery.

7. Write down what you need to see next

Define the evidence that would restore confidence or confirm that the concern is becoming structural.

This turns a vague feeling into a set of conditions you can monitor.

Three ways to describe the state of a thesis

An investment does not need to be treated as either completely healthy or completely broken.

A more useful approach is to recognize three broad conditions.

The thesis remains supported

The main drivers are developing broadly as expected. Temporary problems may exist, but the central evidence remains intact.

The thesis deserves closer monitoring

One or more assumptions are under pressure. The concern is meaningful, but the evidence is not yet broad or persistent enough to reach a firm conclusion.

The thesis has materially weakened

Several central assumptions have deteriorated, the problems are persisting, and the company is no longer developing in a way that resembles the original case.

These descriptions are not instructions to buy or sell.

They provide a clearer way to organize the evidence and decide how much attention the holding deserves.

Monitoring one company is manageable

Following these changes across a full portfolio is much more difficult.

Each company reports on a different schedule. Some changes appear in earnings results. Others show up through estimate revisions, competitor performance, management commentary, or economic conditions.

That is why many investors rely on price alerts.

Price alerts are useful for showing that the market is reacting. They do not explain whether the underlying business evidence has changed.

Thesis monitoring requires following the reasons behind the investment.

How QuarterlyIQ approaches a weakening thesis

QuarterlyIQ helps investors monitor the substance of the companies they own and research.

For covered stocks, we organize the evidence around questions such as:

- What changed?

- Is the change temporary or persistent?

- Which part of the thesis does it affect?

- Are several signals confirming one another?

- Does the evidence remain consistent with the original investment case?

- What should be watched next?

The purpose is not to predict the next movement in the stock or issue a buy, hold, or sell rating.

It is to make meaningful changes easier to recognize before they disappear into the noise of daily market activity.

Explore the QuarterlyIQ stock research section to review covered companies.

The takeaway

A weakening investment thesis usually does not announce itself clearly.

It appears through several smaller changes:

- Growth begins slowing

- Margins remain under pressure

- Estimates move lower

- Management misses commitments

- Competition becomes more effective

- Cash flow weakens

- Valuation remains demanding

Any one of these may be temporary.

Several of them persisting together may tell you that the company is no longer developing the way you originally expected.

Keep the original thesis written down.

Review the evidence in context.

Look for patterns rather than perfection.

Most importantly, allow the facts to update the story instead of allowing the story to explain away every new fact.

For the foundation behind this process, read What Is an Investment Thesis? A Simple Framework for Investors.

For a related decision framework, see When Should You Sell a Stock? A Thesis-First Framework.

For informational purposes only. Not investment advice. QuarterlyIQ provides descriptive, rules-based analysis of company fundamentals and does not recommend buying or selling any security.